Balance Sheet

Would you like to invest your money? Get in touch with an expert:

The balance sheet is the financial statement of a company. A balance sheet provides a summary of the assets, liabilities, and shareholders’ equity of a company at a given point in time. Therefore, a balance sheet is a financial statement that shows what a company owns and owes at a particular point in time. Shareholders' equity is also shown on the balance sheet.

There may be different parties responsible for preparing the balance sheet depending on the company. For small private companies, the balance sheet may be prepared by the owner or an accountant of the company. Medium-sized private companies may prepare their own financial statements and then have them audited by an external accountant. Public companies, on the other hand, are required to be audited by external accountants and must also ensure that their books are maintained to a much higher standard.

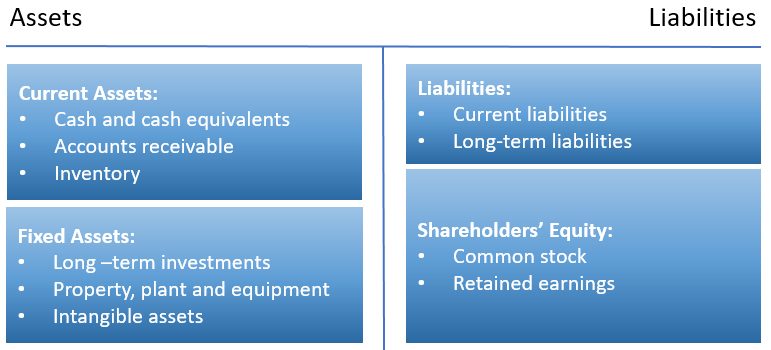

The following figure shows a balance sheet. There are

two sides of the balance sheet, the asset side and the liability side. On the asset side, there are current assets and fixed assets, and on the liability side, there are debts (also referred to as liabilities) and shareholders’ equity. Each of these categories is comprised of several smaller accounts that provide a breakdown of the financial details of a business. Depending on the type of business, these accounts may vary widely by industry. However, there are some common components that investors and analysts are likely to encounter.

The amount of assets and liabilities is always in balance. The company must pay for all things that it owns. A company may obtain capital by taking out loans (liabilities) or by receiving funds from investors (shareholders’ equity). For example, a company might borrow CHF 50,000 to purchase production machinery (tangible assets). On the assets side of the balance sheet, the fixed assets item would increase by CHF 50,000. On the liabilities side, the liabilities increase by CHF 50,000. This results in an increase of CHF 50,000 in the balance sheet totals of the assets (assets side) and the liabilities side. Thus, the assets and liabilities remain in balance.

Balance Sheet Components

Assets

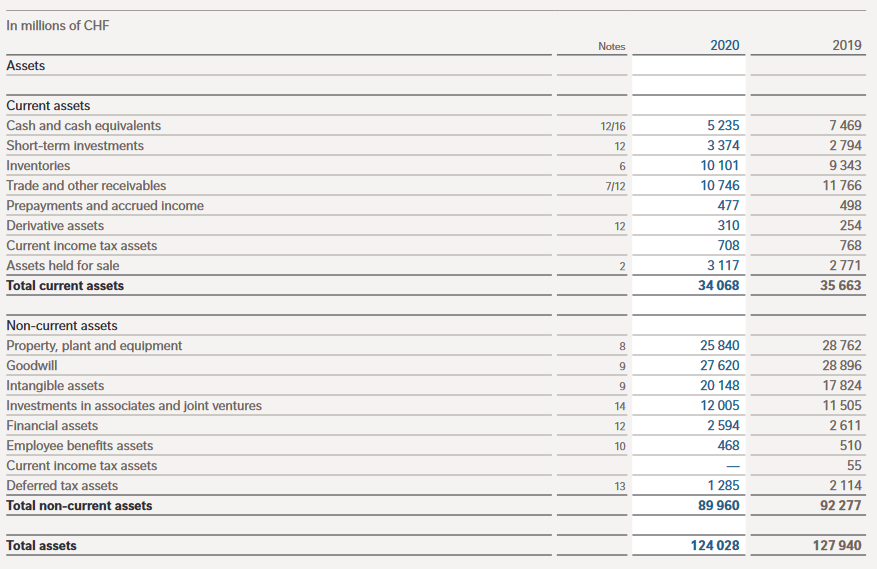

The following figure shows the assets side of Nestlé's balance sheet for 2020. Accounts are arranged in descending order based on liquidity criteria. The current assets are ranked first because they can be converted into cash (liquidated) more rapidly than the non-current assets.

The Asset Side of the Balance Sheet of Nestlé 2020 – Before Appropriations

Source: www.nestle.ch

Cash and cash equivalents are the most liquid assets. Short-term investments are, for example, shares traded on the market. Inventories are all goods available for sale. Trade and other receivables refer to money owed to the company by customers. As some customers may not be able to pay their debts, this may include an allowance for doubtful accounts. Prepayments and accrued income are expenses recognized in the next reporting period that the company will already pay in the current reporting period, for example, insurance policies, advertising contracts, or rent. Derivative assets are financial instruments with a limited term whose value is based on the value of the underlying item (e.g. shares). Nestlé's assets held for sale for 2020 consist mainly of the Nestlé Waters business in North America. The business has been classified as held for sale. The sale agreement was signed on February 16, 2021 and the divestiture should be completed during the first half of 2021.

Non-current assets, which are also referred to as fixed assets, are securities that cannot be liquidated in the next year.

Property, plant and equipment includes, for example, machinery, land and buildings. The definition of

goodwill

is somewhat more extensive. In simple terms, goodwill is the difference between the purchase price paid for a company (e.g., stock market capitalization) and the net asset value determined by accounting.

Intangible assets comprise non-physical (but nevertheless valuable) assets such as intellectual property. These assets are generally only included in the balance sheet if they have been acquired and not developed internally. This means that their value can be undervalued (by not including a globally recognized logo, for example) or equally overvalued.

Liabilities

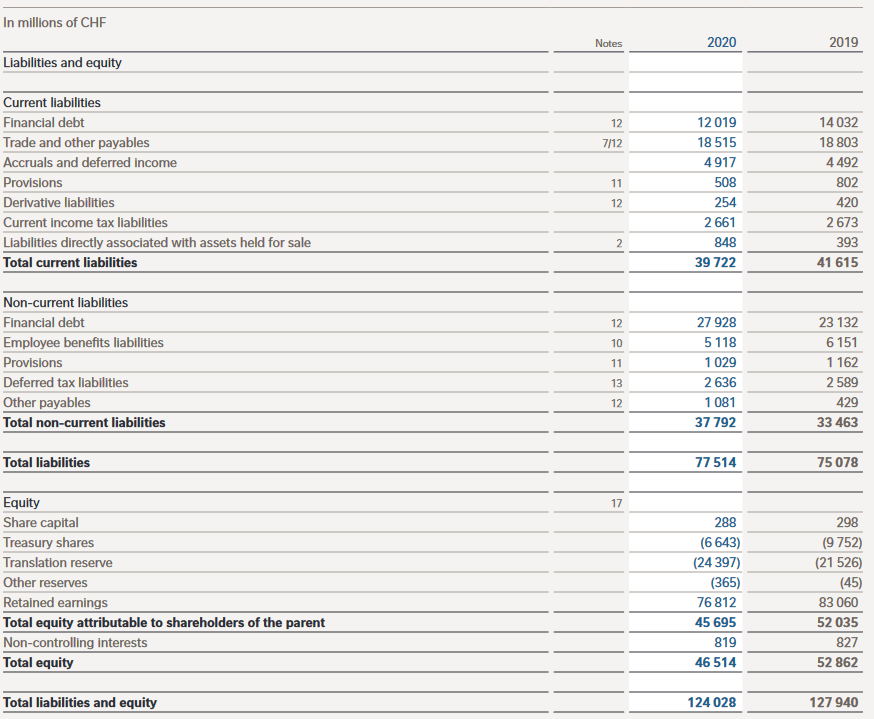

The following figure shows the liabilities side of Nestlé's balance sheet for the year 2020. As with the assets side, the accounts are arranged according to the liquidity criterion. Since current liabilities are due earlier than non-current liabilities, they are listed first in the balance sheet.

The Liability Side of the Balance Sheet of Nestlé 2020 – Before Appropriations

Source: www.nestle.ch

A current liability is debt that a company owes to third parties. Invoices owed to suppliers, interest on bonds, rent, utilities, and outstanding salaries are examples of short-term liabilities.

A non-current liability is defined as the amount of interest and principal owed on bonds issued. Pension liabilities refer to the money that a company must pay into its employees' pension accounts. A deferred tax liability is the amount of taxes accrued but not paid until a later date. Additionally, this figure compensates for differences between financial reporting requirements and how taxes are calculated, for example, in depreciation calculations.

Equity refers to the money owed to the owners of a company or its shareholders. It is often referred to as net assets, as it represents the total assets of a company less its liabilities or debts to non-shareholders. Treasury shares refer to shares that have been repurchased by a company. They can be sold at a later date to raise cash or to prevent a hostile takeover. Additionally, stock corporations are required to allocate 5% of their profits to the legal reserves until the legal reserves total 20% of their share capital.

Fundamental Analyses and the Balance Sheet

Balance sheets, income statements and cash flow statements

are also used for fundamental analyses. It may be beneficial to use key performance indicators in this context. Because the balance sheet is only a snapshot of a company's financial situation, it is usually necessary to analyze the balance sheets of several years back (e.g., up to 10 years ago). As a result, investors can gain a better understanding of the company. For example, the debt-to-equity ratio is an easy indicator to read on the balance sheet.

The balance sheet contains a lot of information for investors and analysts. Unfortunately, the balance sheet is only a snapshot. Thus, only the difference between certain points in time can be analyzed. According to this perspective, the past does not necessarily predict the future. In addition, there are different accounting systems or standards. Inventories and depreciation are handled differently, which affects the reported figures. This situation gives management the opportunity to manipulate the numbers in their favor and also makes it difficult to compare balance sheets between companies, even if they are in the same industry. In making investments, experts such as analysts and well-trained wealth managers are aware of these pitfalls of company analysis and can take them into consideration.

Would you like to invest your money?

Speak to an expert.

Your first appointment is free of charge.